April 13, 2024

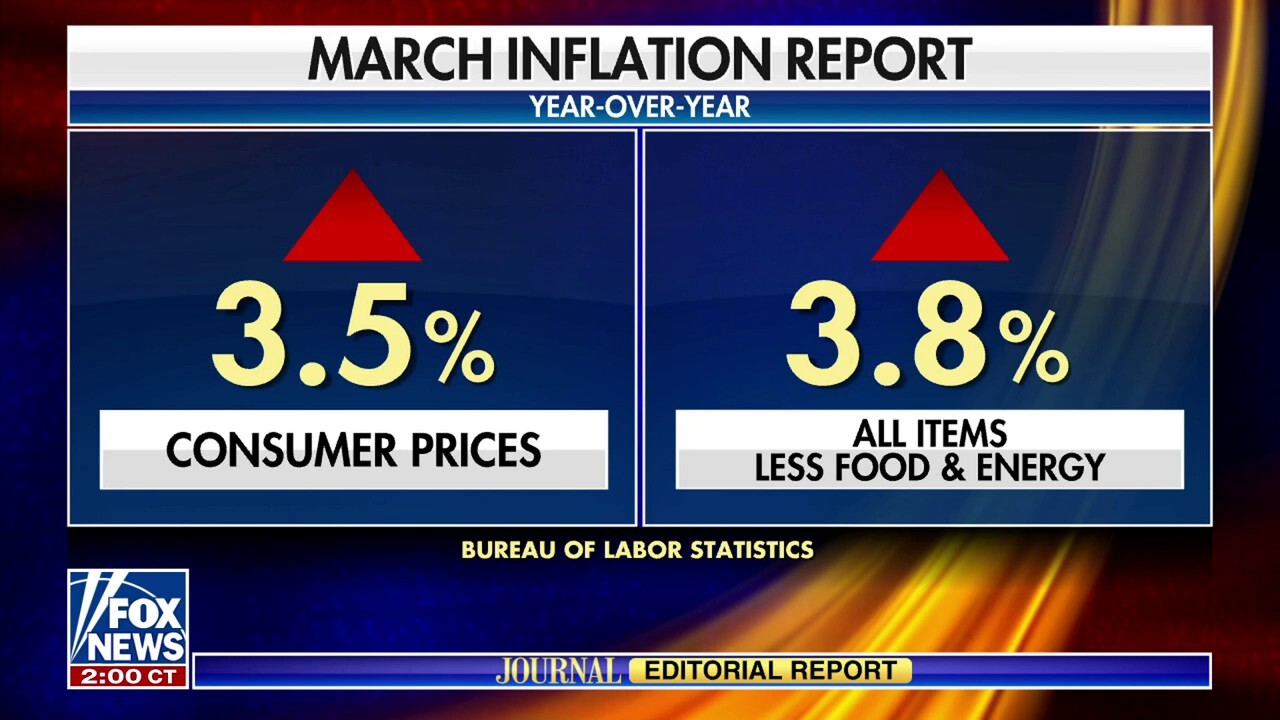

Inflation messes with Joe Biden's presidency

'Bidenomics' still has no answers for high prices.

The Journal Editorial Report Videos

Full Episodes

April 13, 2024

The Journal Editorial Report - Saturday, April 13

April 06, 2024

The Journal Editorial Report - Saturday, April 6

March 30, 2024

The Journal Editorial Report - Saturday, March 30

March 23, 2024